Seven Signs of a Successful DIY Investor

It’s surprising what people will tell you when they find out you’ve switched from a career in tech to financial planning. I’m a big cycling fan, and I’ve had numerous long conversations with friends about the pros and cons of DIY investing vs. Outsourcing during our rides together. I consider them very thoughtful and intelligent, and they’ve mostly been successful with their portfolios ranging from about $2M to $20M. Most are retired now. About half were DIY investors, and the other half outsourced the work. Here are my observations from those conversations.

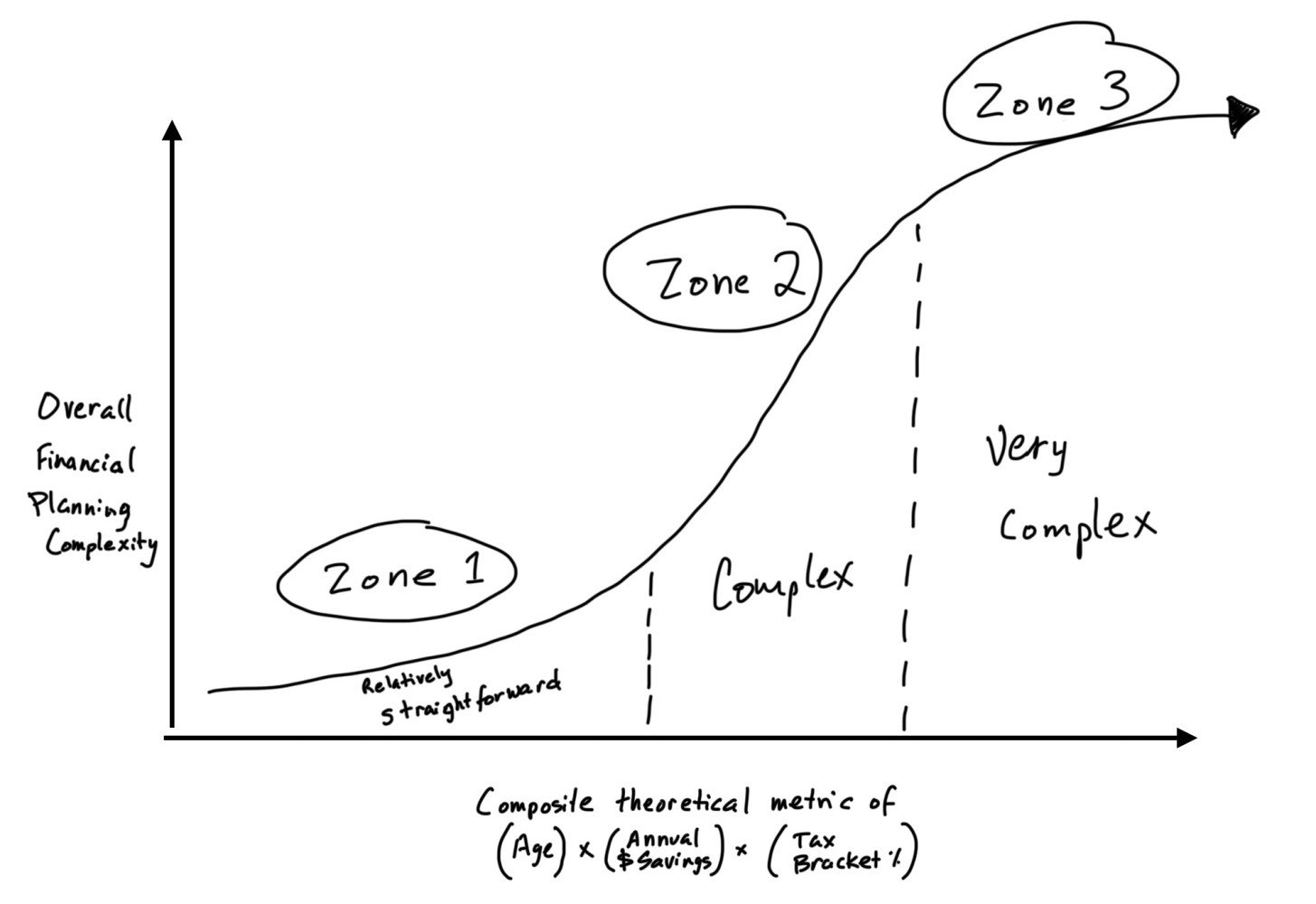

Planning Complexity

First, we all agreed that having a well-designed investment portfolio beats stuffing cash under the mattress or listening to Jim Cramer. The combination of Nobel-prize-winning modern portfolio theory insights, with the complexity of the financial markets and the tax code nowadays, multiplied by the fact that small decisions can have significant long-term ramifications due to compounding over decades, means that curating a retirement portfolio over 30–40-year career requires some genuine expertise. Not to mention drawing down that portfolio during retirement (which is even more complex). The sketch below illustrates what I have in mind:

As your age, income, savings and tax bracket increase, the overall complexity of your financial planning needs increases. It’s easier to DIY in Zone 1 and much harder in Zone 3. The job is easier when we’re young, in a low tax bracket, and without much annual savings, but it quickly gets more complicated as these variables rise.

Pick One

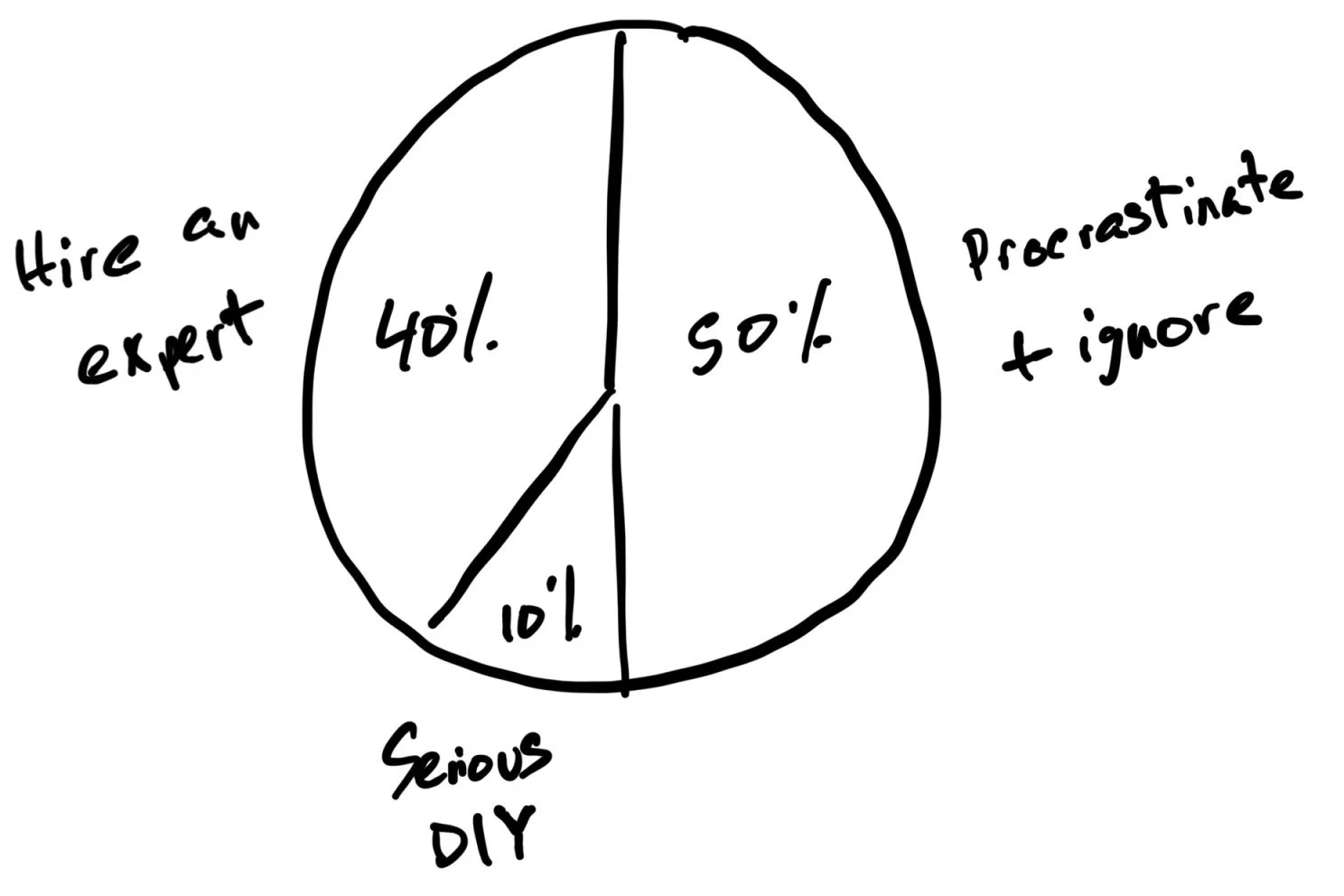

When it comes to managing retirement assets, people seem to fall into three decision buckets (irrespective of what zone they’re in):

1. Become an expert

2. Outsource to an expert

3. Procrastinate-and-Ignore

Based on the industry stats I’ve seen, the following breakdown is roughly accurate:

Busy tech professionals are easily smart enough to become experts if they choose to, but most lack the time or interest. Some may dabble, but they don’t develop real expertise. According to my distinctly non-scientific survey of coworkers in tech, approximately half of the 30 to 55-year-olds in this field fall into what I refer to as P&I: Procrastinate-and-Ignore. I understand. Tech is a demanding career that consumes much of our mental energy and free time. When you add family, friends, hobbies, cooking, exercise, and more, there’s barely any time left.

The result is often a mishmash portfolio of assets that don’t make sense individually, don’t fit into the overall strategy, and may be held in the wrong tax locations. The portfolio structure has no logical rationale. The best of these P&Is will probably use target date funds, and in zone 1, I think those make sense. However, as a person moves into Zone 2, tax issues begin to degrade the appeal of target date funds. As someone moves into Zone 3, the benefits of sophisticated tax planning become much more significant. Zone 3 is when you’re looking at social security optimization, Roth conversions, trusts, custom indexing, exchange funds, concentrated positions, and other things that are challenging to DIY.

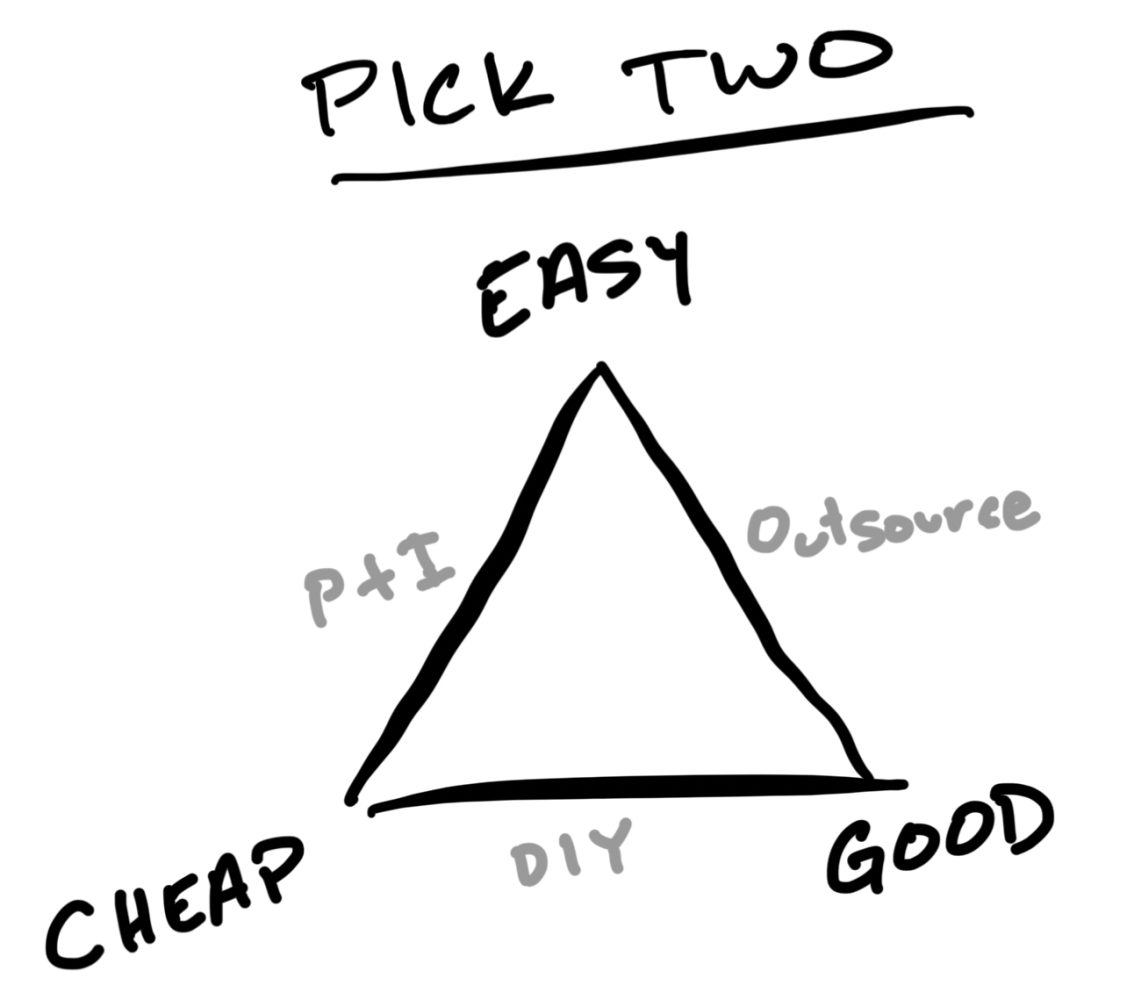

Choosing a Path

Each of these three choices, whether conscious or not, forms from a classic decision triangle that looks like this. In this decision, you can only choose two of the three options:

Cheap + Good = Serious DIY Investing

Easy + Good = Outsource to a Professional

Cheap + Easy = Procrastinate & Ignore

Opportunity Cost [Cheap + Good = Serious DIY]

This article is about DIY and how to do it well. It requires time and attention. Time is a precious commodity, at least as valuable as cash.

For a household earning, let’s say, $250k/yr, their time is worth about $80/hour after taxes. My experience doing DIY in zone 2 on the complexity curve cost me, on average, 10-15 hours a quarter (reading, using software tools, tracking, rebalancing, etc.). For someone at $250k/year, that equates to a breakeven point around $4,800/year after taxes. If they need planning but don’t intrinsically enjoy the activity, outsourcing makes sense if they can do so for less. And that math assumes zero incremental advantage of using a professional vs. DIY, so the actual value is probably higher.

Opportunity cost is why we outsource so much nowadays: healthcare, legal issues, taxes, car repairs, house cleaning, yard maintenance, etc. Yes, if I really wanted to, I suppose I could eventually figure out how to do those things myself, but the math doesn’t add up. So, do what you love, what is intrinsically important to you, or what you’re good at, and outsource the rest.

Procrastinate-and-Ignore [Cheap + Easy = Not Good]

Many people unconsciously fall into this branch of the decision without realizing it. It’s unfortunate because spending years or decades in this camp can really hamper eventual retirement success. Several reputable sources have studied the long-term impact of the P&I decision.

According to Morningstar's latest “Mind the Gap 2024” research paper, mutual fund and ETF investors earned an average of 6.3% per year over the past decade, while the funds they invested in returned 7.3%. What gives? The 1% represents the "oops, I bought or sold at the wrong time" tax. On average, investors do not truly buy and hold across the trillions of dollars invested in funds. Many claim to do so, but they often become anxious when times get tough, they sell, and fail to re-enter the market quickly enough. As Warren Buffet explains, you must make two sequentially correct decisions to time the market correctly: when to exit and when to re-enter. Even if you get the first decision right, without getting the second one right, you lose. And you’re competing against other global investors to do it moments before they do. Good luck with that.

Vanguard, that bastion of self-managed, low-cost investing, investigated what leads to this gap in a widely reported study from 2022[1]. Their research confirmed the results from a previous 2019 Envestnet paper, so the results weren’t surprising. They found

“…the advantage of outsourcing to an expert over procrastinating and ignoring results was between 0.44% - 4.2% of incremental return each year.”

They implied it’s unlikely that most people are doing so poorly that they’d gain the complete 4.2% improvement by outsourcing, but they felt a 3.0% improvement was in the realm of reason. Lest we think 3% compounded annually isn’t much, over 20 years, the gap expands to $800,000 on a one-million-dollar starting portfolio! That’s why Albert Einstein called compounding the 8th wonder of the world. This gap, compounded over the years, overwhelms the relatively small cost of outsourcing to avoid that gap. And that math doesn’t account for the cost of the time incurred by the DIY investor.

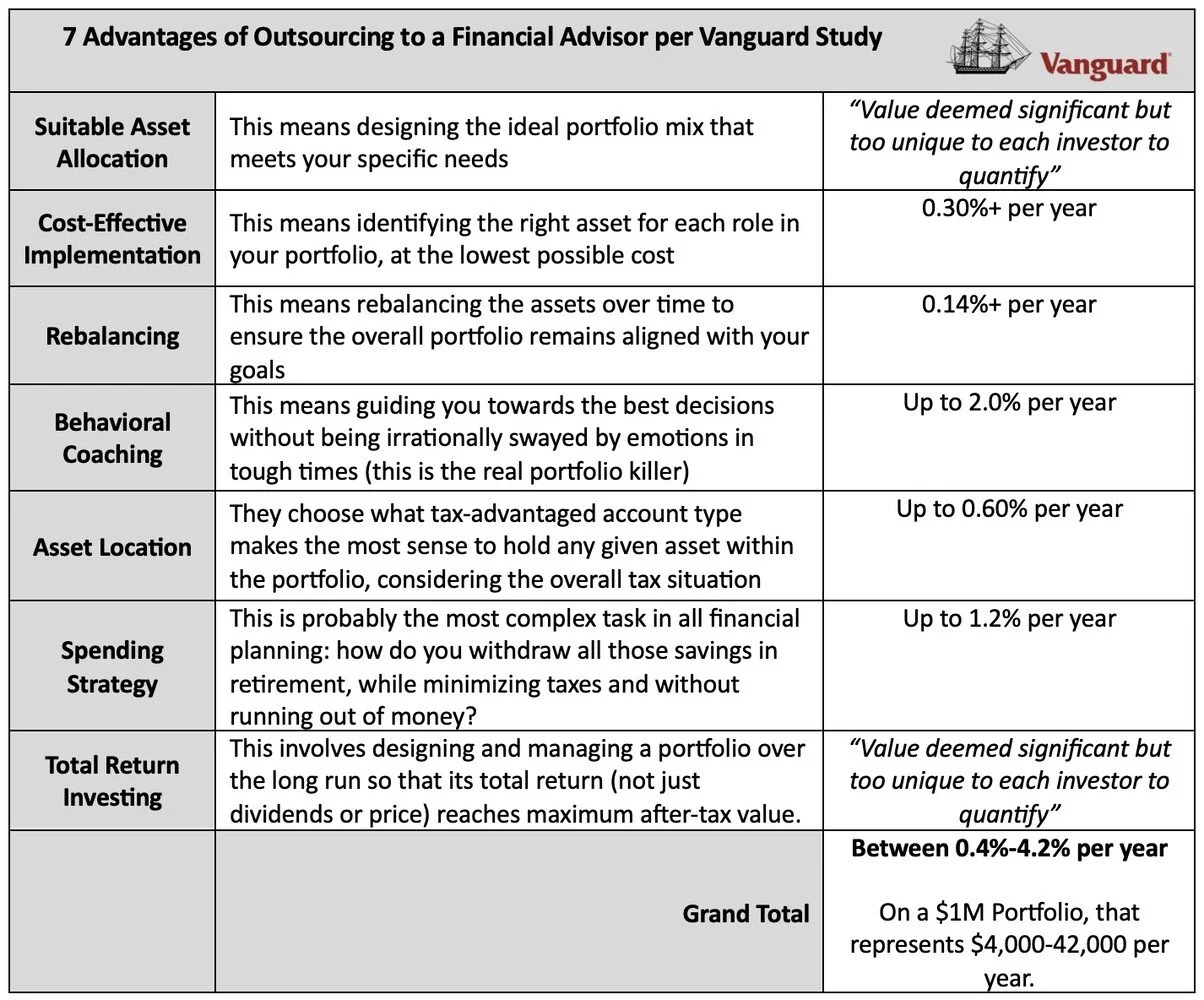

What Good Outsourcing is Supposed to Look Like

Vanguard’s paper found that a good advisor helps close the gap and deliver incremental value over P&I by providing seven key advantages:

Behavioral Coaching: The Biggie

Behavioral coaching was the single most significant source of value they identified. This matches Morningstar’s Mind the Gap study. A good advisor brings a neutral 3rd party perspective and helps take the emotion out of financial decisions. When it comes to investing, for most of us, our worst enemy is ourselves. Poor investing decisions have a moderate impact during bull markets. A rising tide lifts all boats, even the leaky ones. But the real value comes when all hell breaks loose on Wall Street and the bear market comes. We’ve had an incredible run for the past 15 years, so many people have forgotten how hard it is to stand firm while watching a hard-earned portfolio shrink into thin air, month after month. We should all be humble enough to admit we’re prone to emotion-led trading –that’s what the Morningstar data shows.

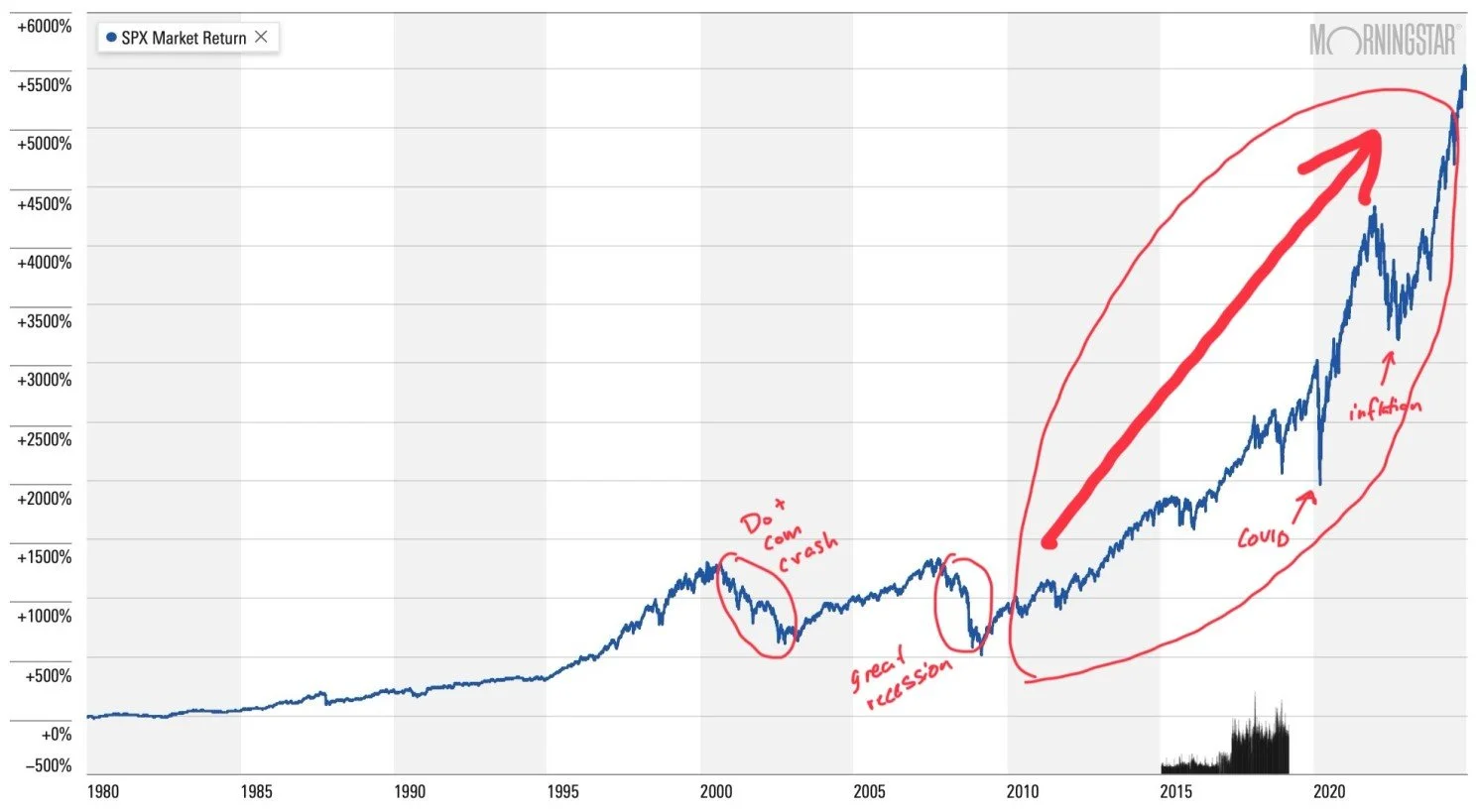

Except for a few brief shocks, the stock market has been going up consistently since 2010

So, respect your future self: You can’t predict what you’ll do when the next bear market hits. But that’s exactly when you need to have an iron stomach. Those who remain steadfast in tough times get richly rewarded in the long run, but it’s incredibly difficult. Back in 2008, I forced myself to methodically rebalance my allocation and continue dollar-cost averaging no matter how far the market dropped. It was challenging because I constantly worried, “What if this time it’s different? What if this is the start of the next great depression? Is this the biggest mistake of my life?”

The last time I’d experienced such a bear market, during the bottom of the dot com crash of 2000, I’d sold in a panic and regretted it for the next eight years. I thought I was a buy-and-hold investor who was rational and unemotional, but when the market collapsed, I found I wasn’t ready for it. Thank goodness I didn’t do that again in 2008 because that simple decision to continue investing no matter what contributed to about half of my retirement portfolio today. The point is that ten years of steady, impartial investment coaching from a good advisor can pay for itself in a single moment at the very worst of times.

Seven Signs You’re Doing DIY Right

So, with all that said, what does it take to DIY in a serious manner worthy of how hard you worked to earn and save those dollars? I know a lot of successful DIYers who would agree with these and might even expand the list. I spent some time on the phone with other successful DIYers to validate these. We all had different ways of saying what are essentially seven signs that someone is doing DIY right:

1. Enjoyment: They enjoy discussing financial topics and have a curious, maker-mindset. If someone’s eyes glaze over when asked about personal finances, that's fine, but maybe DIY isn't their ideal path. If they don’t enjoy the topic, they’re unlikely to have the energy to do this well over the long term.

2. Serious Learning: They’re reading 3-4 books yearly on the topic and they’re interested in the fundamentals of investing. They don’t get distracted by the latest investment “fads”. All serious financial writing eventually gets published in books or academic papers. Although they may start with the basics, they quickly go deeper than financial counseling authors like Ramit Sethi. They read fundamental books like “Stocks for the Long Run 6th Ed.”, “A Random Walk Down Wall Street, 13th Ed.”, “Retirement Planning Guidebook 2nd Ed.” and “Asset Allocation- 5th Ed.” Continuous learning is mandatory because the world of finance and taxes is changing so fast. These people understand the fundamentals of asset classes, portfolio design, and asset allocation. They avoid pop-finance sources on social media, podcasts, or television, knowing those are primarily for entertainment. They avoid books written by people who use them as platforms to sell other things.

3. Tax Planning: They understand their federal, state, and capital gains tax brackets and how to minimize the taxes they pay. They know how much room they have left in each bracket, and they optimize asset selection and placement with tax rates in mind. They know where to hold their fixed income and when to choose munis over treasuries. They may have started with basic tax planning books like The Overtaxed Investor and then progressed to more intricate tax planning concepts. Provided they have the savings capacity, they consistently contribute to backdoor Roth and mega-backdoor Roth plans. They also use Health Savings Accounts as triple-tax-advantaged long-term retirement savings vehicles.

4. Serious Tools: Simplistic, free retirement planning calculators are primarily marketing tools, so they happily pay for serious retirement planning tools[2] and take the time to learn how to use them. A friend who retired from tech in his early fifties told me he spent two years becoming a Pralana expert, starting with a solid week to grasp it and program it initially, then 1-2 hours per week since then. These folks run their own portfolio analyses, Monte Carlo simulations, and tax planning. They have a good sense of their safe withdrawal rate and when they can retire. If they’re over 50, they can tell you their target retirement or career transition date and what it will take to get there.

5. Planning: They follow a well-thought-out investment policy that dictates asset allocation, location, and rebalancing strategies. They’re happy to tell you all about it if you ask, and they are rigorously disciplined in executing their plan. As part of this discipline, they periodically liquidate ESPP and vested RSU shares or options (if they hold them, they have a good reason for doing so).

6. Budgets: People usually rely on an expense or budget-tracking app. I don’t know if this necessarily leads to financial success, especially for innately frugal individuals, but anecdotally, there seems to be a high correlation. People who care about their money track it.

7. Humility: DIYers take a humble approach to their plans, seeking diverse insights because they don’t know what they don’t know. They’re open to advice and better ideas. This fits in with the curious mindset. They’re looking for others to review and comment on their portfolio. One very successful person I spoke to (you know who you are) told me:

“I feel good about my asset allocation, but I use a third party to review it every year and give me feedback. Sometimes I take their advice, sometimes I don’t, but I always ask for input...I used to think financial planners were only interested in selling me stuff, but I’ve come to appreciate the value of feedback from a professional.”

Okay. If that sounds like a lot, it is. Wade Pfau PhD, a well-known academic in this space, puts it this way:

“…. Those with high self-efficacy believe they can be successful with personally implementing the steps outlined in this book. These individuals will not procrastinate, will view themselves as having the resolve to overcome behavioral hurdles, and can cope with the natural stressors of aging. Though inconclusive, the fact that you have made it this far into the book suggests you may have high self-efficacy for retirement income.”[3]

I believe it’s entirely reasonable to DIY your retirement planning if you have the time and the interest. I did it successfully, and so have many others, but it's not for everyone. Please do yourself a favor and figure out where you sit on that decision triangle, then do something about it. Whatever you do, don’t default to procrastinate-and-ignore. Over the long term, this decision will significantly impact your life, so the sooner you make it consciously, the better.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and does not constitute specific financial, tax, or legal advice. All investing involves risk, including the potential loss of principal. Market data and statistics cited are believed to be accurate as of the date of publication, but are subject to change. Please consult with a qualified financial professional to discuss your individual circumstances and risk tolerance before making any investment decisions.

[1] Vanguard “Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha” Figure 1, July 2022. “…We believe implementing the Vanguard Advisor’s Alpha framework can add up to, or even exceed, 3% in net return…”

[2] The most serious tools currently available to consumers I’m familiar with are MaxiFi and Pralana. Unfortunately, most financial planning software is only offered commercially, and the licenses are expensive (Right Capital, eMoney, MoneyGuidePro, Holistiplan tax software, etc.). I suppose that’s because the market for serious DIY consumers isn’t very big.

[3] page 473, Pfau, Wade. Retirement Planning Guidebook: Navigating the Important Decisions for Retirement Success (The Retirement Researcher Guide Series).